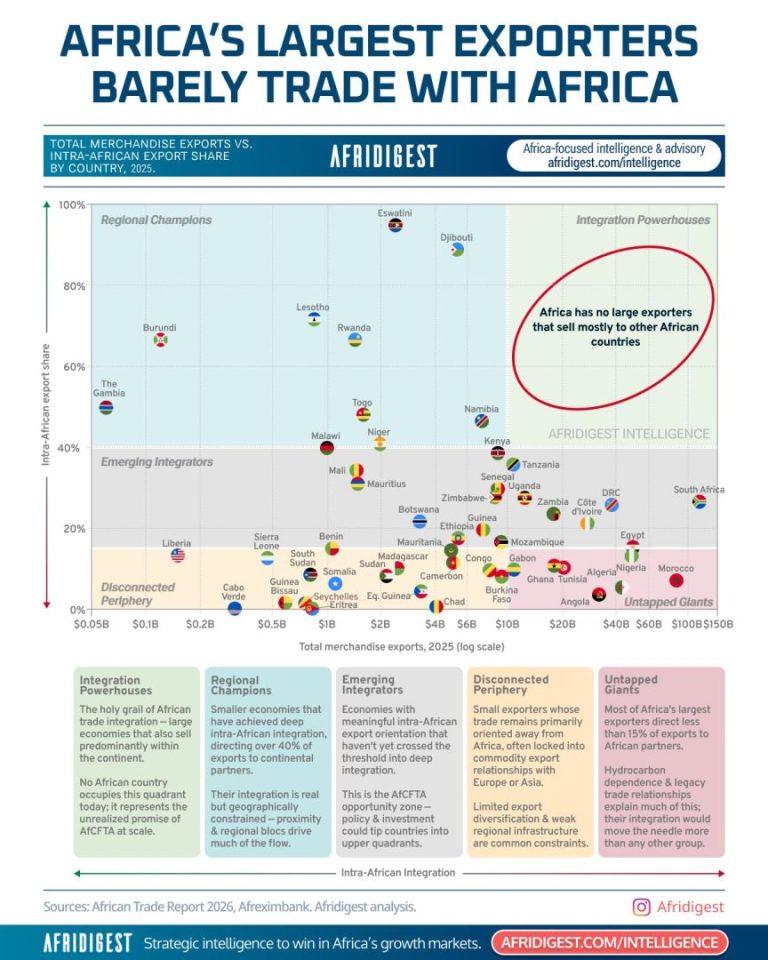

Africa’s biggest exporters are also some of the least Africa-facing.

That’s why intra-African trade is just ~15% of total African trade, compared to roughly 60% intra-regional trade for both Asia and Europe.

This chart maps total merchandise exports (i.e. physical goods, not services) against intra-African export share — because a country can be a trade giant and still barely sell to its neighbors.

What it shows:

- Untapped Giants: Nigeria, Egypt, Morocco, Algeria, Angola, et al. — combined these countries generate over 45% of all African merchandise exports. But because their export profiles are structurally hardwired away from Africa towards global oil markets, European nearshoring, or the Arab world, they account for just ~25% of intra-African exports.

- Disconnected Periphery: Liberia, Sierra Leone, Cabo Verde, Guinea-Bissau, et al. — smaller exporters whose economies are locked into exporting raw commodities out of Africa or navigating structural challenges that break regional trade links.

- Emerging Integrators: South Africa, Kenya, Tanzania, Senegal, Uganda, Zambia, et al. — dual-engine export economies that operate as regional manufacturing or agricultural anchors for their neighbors while simultaneously shipping high-value primary resources to global markets. This is the immediate AfCFTA opportunity zone for deeper integration.

- Regional Champions: Eswatini, Lesotho, Rwanda, Burundi, Djibouti, et al. — small exporters, but over 40% of what they sell goes to continental partners. The integration is real but driven by proximity, regional trade blocs (like SACU), and lack of large-scale raw commodity exports to global markets.

- Integration Powerhouses: None — No large exporter in Africa today sells at scale predominantly to other African countries. Until industrialization on the continent advances with enough domestic refining, processing, and manufacturing capacity to absorb and transform local raw materials, scale and deep regional integration will remain structurally incompatible.

| Country | Global Export Profile | Dominant Global Buyers | Why the Intra-African % Stays Under 15% |

|---|---|---|---|

| Nigeria | Crude Oil | India, EU, North America | African neighbors lack the refining capacity to buy its crude. |

| Egypt | Manufactured Goods, Gas | Middle East, EU | Historically bound to Middle Eastern and Mediterranean trade pacts. |

| Morocco | Automobiles, Aerospace, Fertilizers | European Union | Factories are structurally wired directly into European supply chains. |

| Algeria / Angola | Oil and Natural Gas | Europe, China | Fixed pipelines and global tankers send energy entirely out of Africa. |

| Country | Primary Export Footprint | Why It Overlooks Africa |

|---|---|---|

| Liberia / Sierra Leone | Iron Ore, Gold, Diamonds | Raw industrial materials sent exclusively to global factories. |

| Cabo Verde | Fish, Tourism Services | High maritime costs to mainland Africa; relies on European shipping routes. |

| Guinea-Bissau | Raw Cashew Nuts | ~90% of exports are raw cashews, shipped directly to India and Vietnam for processing; poor ‘trade complementarity’ with neighbors; little industrial processing capacity. |

| Somalia / Sudan | Livestock, Crude Oil | Hampered by active conflict, unstable infrastructure, and security risks. |

| Eritrea | Gold, Zinc | Widely considered one of the most politically & economically isolated countries in the world; only African Union member state that has not signed the AfCFTA agreement. |

| South Sudan / Chad | Crude Oil | Bypasses African markets due to a dearth of regional refining infrastructure. |

| Country | Major Regional Exports (To Africa) | Major Global Exports (To Rest of World) |

|---|---|---|

| South Africa | Machinery, vehicles, processed food, chemicals | Gold, platinum, coal, citrus fruits |

| Kenya | Refined petroleum, manufactured chemicals, cement | Cut flowers, tea, coffee |

| Tanzania | Rice, textiles, construction materials | Gold, raw cashews, tobacco |

| Uganda | Milk, grain, sugar, electricity | Coffee, gold |

| Zambia | Agricultural goods, electricity, copper wires | Raw refined copper, emeralds |

| Senegal | Cement, processed fish, fertilizers | Crude petroleum, gold, phosphoric acid |

| Country | Regional Integration Driver | Why the Intra-African % Runs High |

|---|---|---|

| Eswatini / Lesotho | Southern African Customs Union (SACU) membership | Deep integration with South Africa means manufacturing and agricultural output flows directly across open, duty-free borders. |

| Rwanda / Burundi | Landlocked, neighbor-dependent trade | Lack large-scale global commodity exports (oil, minerals); smaller manufacturing and agricultural sectors rely on trade with the DRC, Kenya, and Tanzania. |

| Djibouti | Regional logistics and transit hub | Service-based economy earns heavily by processing goods flowing through its ports to landlocked neighbors like Ethiopia. |

Africa’s path to prosperity goes through intra-African trade; it’s the kind of trade that creates jobs, develops capabilities, and strengthens economies.

But it requires industrialization — moving away from exporting raw commodities and towards value-added manufacturing and regional supply chains.

While AfCFTA implementation is increasingly emphasized across markets, building industrial capacity must be too.

Ultimately, the continent’s future depends on factories, not just frameworks.

Share: